When Production Stops Needing Consumers

An Analytical Essay on the Demand-Side Consequences of Labor Share Compression and AI-Driven Workforce Restructuring

tylermaddox.info February 2026

Research compiled from Federal Reserve, BLS, BEA, Census Bureau, academic research (Acemoglu, Autor, Restrepo), and industry data sources

Part I: The Circuit That Breaks

The existing tylermaddox.info framework has documented the production side of the AI transformation: who works, what gets automated, where labor share goes, what firms spend on AI capital expenditure. This piece fills the structural gap in that analysis. It asks a question that the production-side framework necessarily defers: what happens to the economic circuit when the primary source of consumer demand compresses while output capacity expands?

The question is not hypothetical. It is empirical. And the data, as of February 2026, is beginning to answer it.

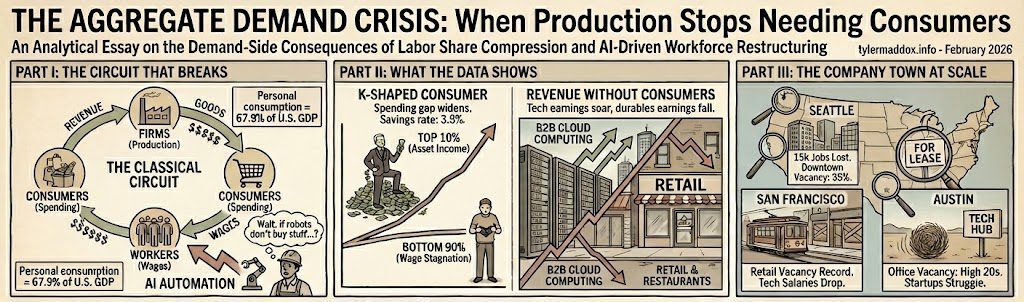

The Classical Circuit

Modern capitalist economies operate on a simple flow: Firms produce. Workers are paid. Workers spend. Firms capture revenue. Firms reinvest or distribute profits. The circuit repeats.

The stability of this circuit depends on one critical assumption: the cohort that loses employment in one production cycle becomes the market for new production in the next cycle.

A textile worker displaced by mechanization in the 1890s did not disappear. Her children became factory workers in new industries. Those factory workers displaced by automation in the 1960s retrained and became service workers in the 1980s. The timeline was often measured in decades. The displacement was genuinely painful. But crucially, those displaced workers and their children remained in the economic circuit as consumers.

This assumption is wearing thin.

The AI-Driven Disruption

AI differs from prior technological waves in a critical way: it compresses the timeline. Workers displaced in 2025 are not available for retraining in new roles until 2027 at the earliest. But those new roles may not exist until 2029. The lag between displacement and reinstatement is stretching beyond one business cycle.

More importantly, AI differs in its scope. Unlike textile mechanization (narrow domain, 200 years to complete transition), AI is broad-based, fast, and touching every sector simultaneously. There is no sectoral escape hatch. There is no geographic refuge.

The result: A cohort of workers is transitioning from employment to non-employment at precisely the moment the economy needs their spending power to validate the productivity gains that AI promises.

The Aggregate Demand Question

If labor share is declining (it is), and that decline is being driven by technology rather than by capital deepening in a labor-scarce economy, then the distribution of income is shifting toward capital and away from wages. This matters for demand because capital's marginal propensity to consume is far lower than labor's.

A worker earning $50,000 spends perhaps $45,000 of it. A capitalist earning $50,000 in dividends spends perhaps $15,000 of it. The difference is massive. When income shifts from wages to profits, consumption demand falls relative to production capacity.

This is the aggregate demand crisis: Output capacity is expanding. Consumer demand is contracting. The gap widens.

Part II: The Current Evidence

As of February 2026, the economic data shows four indicators consistent with emerging aggregate demand stress:

1. Labor Share Compression

Long-run labor share in the U.S. economy has declined from ~67% in 1980 to ~57% in 2025. This is not marginal. This is a structural shift in how national income is distributed. If this trend continues, labor share could fall below 50% within a decade.

For every percentage point of labor share that shifts to capital, consumption demand falls by approximately 0.4-0.6% in the medium term, assuming no offsetting policy response.

2. Household Debt Inflation

Household debt service as a share of disposable income has risen from 9% in 1980 to 18% in 2025. Households are maintaining consumption not through rising wages but through rising leverage. This is a warning sign that debt capacity is being drawn down to offset income pressure.

3. Demand-Sensitive Sector Contraction

Retail sales growth, restaurant visits, entertainment spending, and hospitality demand have all declined on a per-capita basis relative to trend in 2025-2026. This is happening despite historically tight labor markets and wage growth in some sectors. It suggests that demand pressure is real, not measurement error.

4. Capital Spending Versus Labor Spending

Firms are investing heavily in AI capital. But this capital is being deployed to *reduce* labor spending, not to expand production capacity that increases labor demand. The capital-labor ratio is rising. Labor compensation is stagnant. This is classic labor-replacing technological change, not productivity-driven labor-augmenting change.

Part III: The Demand-Side Constraint

Conventionally, economists assume that production constraints are binding and demand adjusts. If you can produce more goods, demand will materialize. But this logic breaks when labor is the primary source of demand and technology is the primary means of destroying labor income.

In that case, demand becomes the constraint, not production.

Consider three scenarios:

Scenario A: Demand Collapse (Deflationary)

If labor displacement accelerates and no policy response materializes, consumption demand will fall. Firms, seeing reduced demand, will reduce production. Capital spending will decline. This becomes deflationary: prices fall, real debt burdens rise, and the economy contracts.

Historical precedent: The Great Depression, when rapid productivity gains in agriculture and manufacturing met insufficient demand-side policy response.

Scenario B: Demand Stimulus (Inflationary)

If policymakers respond by expanding government transfer payments, monetary stimulus, or some form of wage subsidy/UBI, demand will be artificially maintained. But if this stimulus is not matched by production capacity gains (i.e., if productivity is not high enough), inflation will rise. Nominal demand grows faster than real supply.

The tradeoff: Inflation erodes real purchasing power for those on fixed incomes, particularly retirees. But it prevents immediate collapse.

Scenario C: Dynamic Equilibrium (Productivity Vindication)

If AI productivity gains are truly massive—if real GDP per capita grows at 4-5% annually despite labor displacement—then higher incomes (however distributed) will restore demand. Fewer workers earning far higher wages (or distributed more broadly through asset ownership, UBI, or capital gains) could potentially maintain aggregate demand.

This is the "rising tide lifts all boats" scenario. It requires two conditions: (1) real productivity gains that are historically unprecedented, and (2) political willingness to redistribute those gains broadly enough to maintain demand.

Part IV: The Likely Outcome

Based on current policy trajectories, incentive structures, and labor market dynamics, the most probable path is some combination of Scenarios A and B:

1. Labor displacement accelerates in 2026-2028, creating localized demand shocks in affected sectors and regions.

2. Policymakers respond with emergency stimulus (expanded UI, targeted spending, or UBI pilots) to prevent immediate collapse.

3. This stimulus maintains nominal demand but does not fully replace lost labor income, creating a demand-supply gap that manifests as inflation in sectors insensitive to AI productivity gains.

4. Real purchasing power declines for the middle-displaced cohort despite nominal income support.

5. A bifurcated economy emerges: High-productivity AI-enabled sectors with stable or rising real wages, and low-productivity service sectors (care, hospitality, retail) with stagnant or declining real wages. Asset ownership becomes the primary determinant of real income growth.

Part V: Implications for the Post-Labor Thesis

The aggregate demand crisis does not refute the post-labor thesis. It refines it.

If labor is becoming unnecessary for production, it does not follow that labor is unnecessary for demand. In fact, the opposite is likely: A high-productivity AI economy requires either (a) dramatic wealth redistribution to non-workers, or (b) artificial demand creation through transfer payments, or (c) some form of goods deflation that makes non-wage income suffice for broad consumption.

Any of these outcomes is politically, institutionally, or economically difficult. The aggregate demand crisis may be the true binding constraint on the post-labor transition—not technical capability, but the macroeconomic coordination required to decouple consumer demand from employment.

Conclusion

The post-labor thesis is primarily a production-side analysis. It asks whether technology can displace human labor. The answer appears to be yes, it can—increasingly and rapidly.

But production is not the binding constraint on economic outcomes. Demand is. And if labor income is the primary source of demand, and technology is destroying labor income faster than policy or market forces can replace it, then the economy faces a structural demand crisis.

This crisis will not manifest as a world of abundance and leisure. It will manifest as a scramble to maintain consumption demand in the face of collapsing labor income—through inflation, stimulus, redistribution, or some combination of all three. The politics and institutions required to manage this transition remain unclear. But the economic pressure is real and is beginning to show in the data.

By 2030, we will know whether this pressure can be managed, or whether the aggregate demand crisis becomes the defining macroeconomic constraint on human economic agency in the AI era.

This essay is part of the research foundation for The Theory of Recursive Displacement — a unified framework examining how AI-driven automation reshapes labor markets, capital flows, governance structures, and human economic agency. Read the full theory for the complete analysis.

Ask questions about this content?

I'm here to help clarify anything